The Internal Revenue Service, the states and the tax industry urge you to be safe online and remind you to take important steps to help protect yourself against identity theft.

Taxes. Security. Together. Working in partnership with you, we can make a difference. Scammers, hackers and identity thieves are looking to steal your personal information – and your money. But there are simple steps you can take to help protect yourself, like keeping your computer software up-to-date and giving out your personal information only when you have a good reason. We all have a role to play to protect your tax account. There are just a few easy and practical steps you can take to protect yourself as you conduct your personal business online. Here are some best practices you can follow to protect your tax and financial information: 1. Understand and Use Security Software. Security software helps protect your computer against the digital threats which are prevalent online. Generally, your operating system will include security software or you can access free security software from well-known companies or Internet providers. Other options may have an annual licensing fee and offer more features. Essential tools include a firewall, virus/malware protection and file encryption if you keep sensitive financial/tax documents on your computer. Security suites often come with firewall, anti-virus and anti-spam, parental controls and privacy protection. File encryption to protect your saved documents may have to be purchased separately. Do not buy security software offered as an unexpected pop-up ad on your computer or email! It’s likely from a scammer. 2. Allow Security Software to Update Automatically. Set your security software to update automatically. Malware – malicious software – evolves constantly and your security software suite is updated routinely to keep pace. 3. Look for the “S” for encrypted “https” websites. When shopping or banking online, always look to see that the site uses encryption to protect your information. Look for https at the beginning of the web address. The “s” is for secure. Unencrypted sites begin with an http address. Additionally, make sure the https carries through on all pages, not just the sign-on page. 4. Use Strong Passwords. Use passwords of at least 10 to 12 characters, mixing letters, numbers and special characters. Don’t use your name, birthdate or common words. Don’t use the same password for several accounts. Keep your password list in a secure place or use a password manager. Don’t share your password with anyone. Calls, texts or emails pretending to be from legitimate companies or the IRS asking you to update your accounts or seeking personal financial information are generally scams. 5. Secure your wireless network. A wireless network sends a signal through the air that allows you to connect to the Internet. If your home or business wi-fi is unsecured it also allows any computer within range to access your wireless and steal information from your computer. Criminals also can use your wireless to send spam or commit crimes that would be traced back to your account. Always encrypt your wireless. Generally, you must turn on this feature and create a password. 6. Be cautious when using public wireless networks. Public wi-fi hotspots are convenient but often not secure. Tax or financial Information you send though websites or mobile apps may be accessed by someone else. If a public Wi-Fi hotspot does not require a password, it probably is not secure. If you are transmitting sensitive information, look for the “s” in https in the website address to ensure that the information will be secure. 7. Avoid phishing attempts. Never reply to emails, texts or pop-up messages asking for your personal, tax or financial information. One common trick by criminals is to impersonate a business such as your financial institution, tax software provider or the IRS, asking you to update your account and providing a link. Never click on links even if they seem to be from organizations you trust. Go directly to the organization’s website. Legitimate businesses don’t ask you to send sensitive information through unsecured channels. To learn additional steps you can take to protect your personal and financial data, visit Taxes. Security. Together. Also read Publication 4524, Security Awareness for Taxpayers. Each and every taxpayer has a set of fundamental rights they should be aware of when dealing with the IRS. These are your Taxpayer Bill of Rights. Explore your rights and our obligations to protect them on IRS.gov.

Comments

The Internal Revenue Service today reminded eligible employees that now is the time to begin planning to take full advantage of their employer’s health flexible spending arrangement (FSA) during 2016.

FSAs provide employees a way to use tax-free dollars to pay medical expenses not covered by other health plans. Because eligible employees need to decide how much to contribute through payroll deductions before the plan year begins, many employers this fall are offering their employees the option to participate during the 2016 plan year. Interested employees wishing to contribute during the new year must make this choice again for 2016, even if they contributed in 2015. Self-employed individuals are not eligible. An employee who chooses to participate can contribute up to $2,550 during the 2016 plan year. Amounts contributed are not subject to federal income tax, Social Security tax or Medicare tax. If the plan allows, the employer may also contribute to an employee’s FSA. Throughout the year, employees can then use funds to pay qualified medical expenses not covered by their health plan, including co-pays, deductibles and a variety of medical products and services ranging from dental and vision care to eyeglasses and hearing aids. Interested employees should check with their employer for details on eligible expenses and claim procedures. Under the use or lose provision, participating employees often must incur eligible expenses by the end of the plan year, or forfeit any unspent amounts. But under a special rule, employers may, if they choose, offer participating employees more time through either the carryover option or the grace period option. Under the carryover option, an employee can carry over up to $500 of unused funds to the following plan year—for example, an employee with $500 of unspent funds at the end of 2016 would still have those funds available to use in 2017. Under the grace period option, an employee has until 2½ months after the end of the plan year to incur eligible expenses—for example, March 15, 2017, for a plan year ending on Dec. 31, 2016. Employers can offer either option, but not both, or none at all. Employers are not required to offer FSAs. Accordingly, interested employees should check with their employer to see if they offer an FSA. More information about FSAs can be found in Publication 969 , available on IRS.gov.  When you apply for assistance to help pay the premiums for health coverage through the Health Insurance Marketplace, the Marketplace will estimate the amount of the premium tax credit that you may be able to claim. The Marketplace will use information you provide about your family composition, your projected household income, whether those that you are enrolling are eligible for other non-Marketplace coverage, and certain other information to estimate your credit.

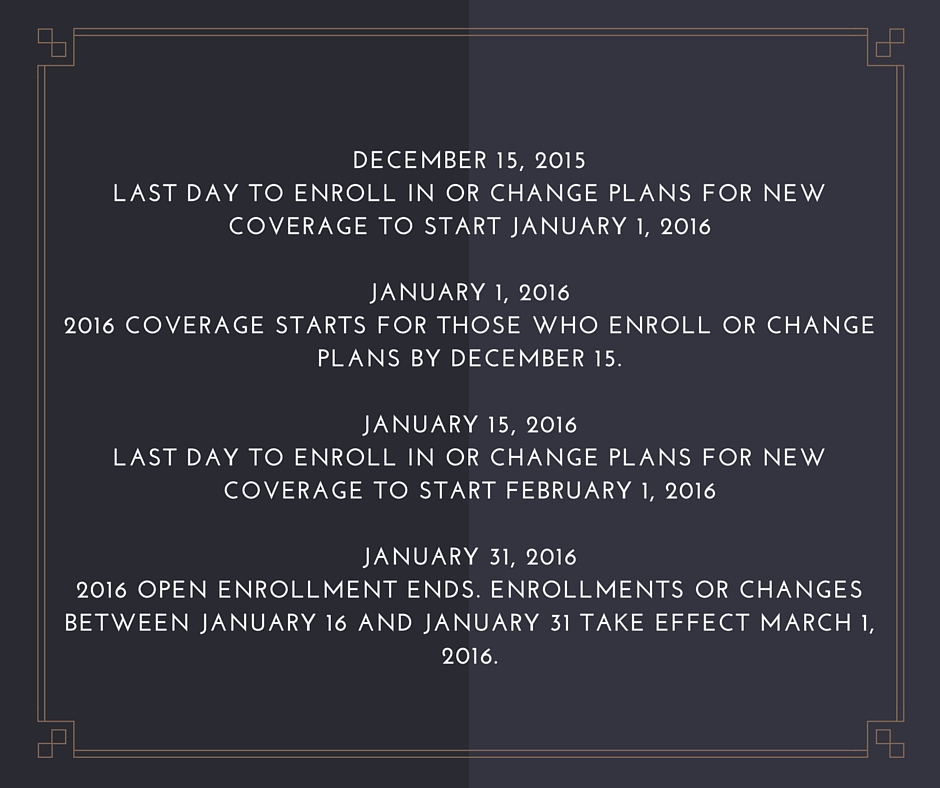

Here are three things you should consider during the Health Insurance Marketplace Open Enrollment period: 1. Advance credit payments lower premiums - You can choose to have all, some, or none of your estimated credit paid in advance directly to your insurance company on your behalf to lower what you pay out-of-pocket for your monthly premiums. These payments are called advance payments of the premium tax credit or advance credit payments. If you do not get advance credit payments, you will be responsible for paying the full monthly premium. 2. A tax return may be required - If you received the benefit of advance credit payments, you must file a tax return to reconcile the amount of advance credit payments made on your behalf with the amount of your actual premium tax credit. You must file an income tax return for this purpose even if you are otherwise not required to file a return. 3. Credit can be claimed at tax time - If you choose not to get advance credit payments, or get less than the full amount in advance, you can claim the full benefit of the premium tax credit that you are allowed when you file your tax return. This will increase your refund or lower the amount of tax that you would otherwise owe. For more information about open season enrollment, which runs through January 31, 2016, visit Healthcare.gov. See our Questions and Answers on IRS.gov/ca for information about the premium tax credit.

The Internal Revenue Service reminds taxpayers that the earlier in the year they check their withholding, the easier it will be to get the right amount of tax withheld.

Besides wages, income tax is often withheld from other types of income, such as pensions, bonuses, commissions and gambling winnings. Ideally, taxpayers should try to match their withholding with their actual tax liability. If not enough tax is withheld, they will owe tax at the end of the year and may have to pay interest and a penalty. If too much tax is withheld, they will lose the use of that money until they get their refund. This is the first in a series of weekly tax preparedness releases designed to help taxpayers begin planning to file their 2015 return. When Should Taxpayers Check their Withholding?

Use the IRS Withholding Calculator on IRS.gov. This easy-to-use tool can help figure the taxpayer’s federal income tax withholding so their employer can withhold the correct amount from their pay. This is particularly helpful if they've had too much or too little withheld in the past, their situation has changed, or they started a new job. Taxpayers may also use the worksheets and tables in Pub 505:TaxWithholding and Estimated Tax, to see if they are having the right amount of tax withheld. How to Change the Amount being withheld Events during the year may change a taxpayer’s marital status or the exemptions, adjustments, deductions, or credits they expect to claim on their return. When this happens, taxpayers may need to give their employer a new Form W-4, Employee's Withholding Allowance Certificate to change their withholding status or number of allowances. Generally, taxpayers should give their employer a new Form W–4 within 10 days after either:

Other Considerations

Find more information on this and other tax topics by visiting:www.irs.gov/Individuals. |

AuthorJessica Clark has over 12 years experience in the accounting industry. Archives

November 2016

Categories |

RSS Feed

RSS Feed